The Job Market in 2026 Is Being Reshaped by War, Oil Shocks, and a Hiring Freeze Nobody Predicted

When employers decide to hire or freeze hiring, they post or pull job listings immediately, weeks before those decisions show up in official payroll counts. That’s why real-time job postings data from platforms like JobsPikr leads BLS figures by 3–4 weeks, giving talent intelligence teams a warning of where the labor market is actually heading.

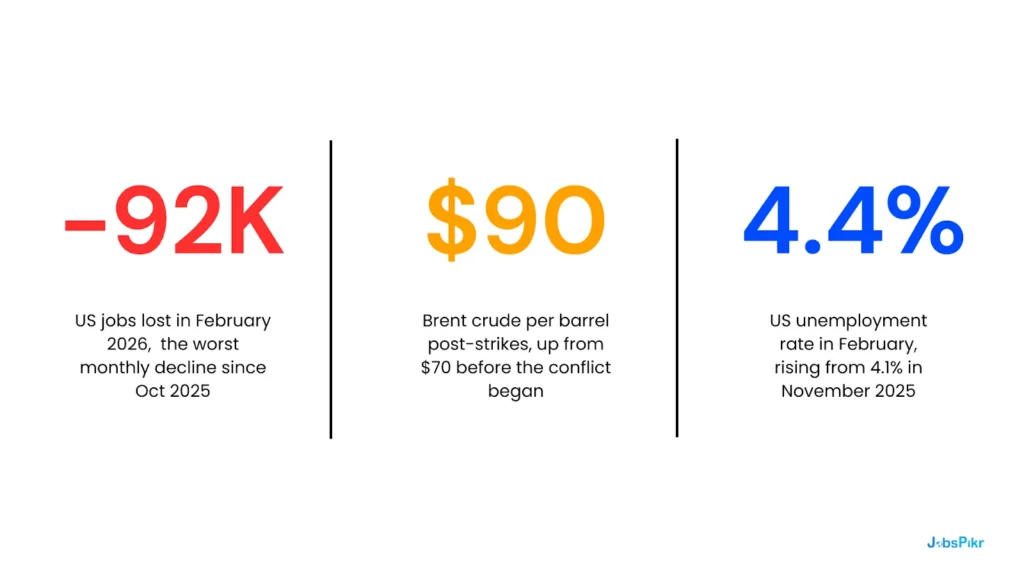

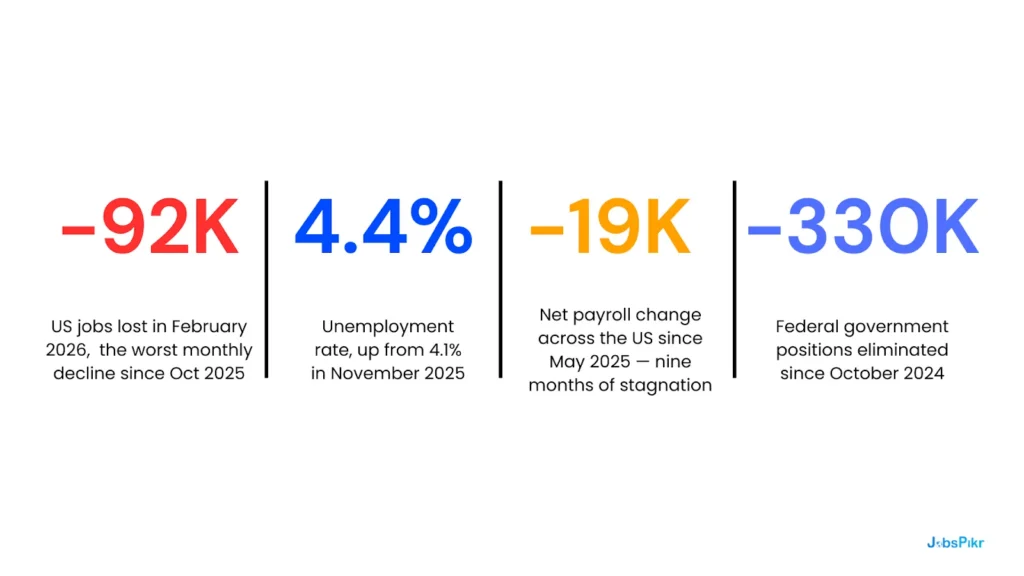

- The US economy lost 92,000 jobs in February 2026: the steepest single-month decline since October 2025, before the US-Israel strikes on Iran even registered in employer hiring decisions.

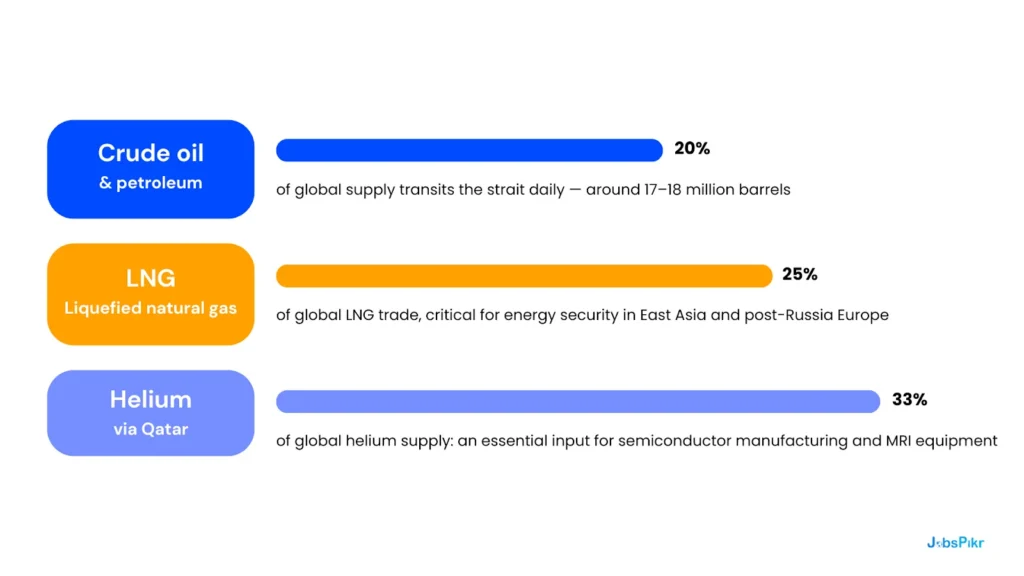

- The conflict has paralyzed shipping through the Strait of Hormuz, the chokepoint for roughly 20% of the world’s oil and LNG supply, sending Brent crude surging from $70 to $90 a barrel in under a week.

- Two job markets are diverging fast: defense, cybersecurity, and renewable energy are surging, while Gulf logistics, hospitality, oil & gas, and trade finance are contracting sharply.

- The Federal Reserve is caught between a softening labor market and re-igniting inflation, making the rate cuts businesses were counting on in 2026 increasingly unlikely to arrive on schedule.

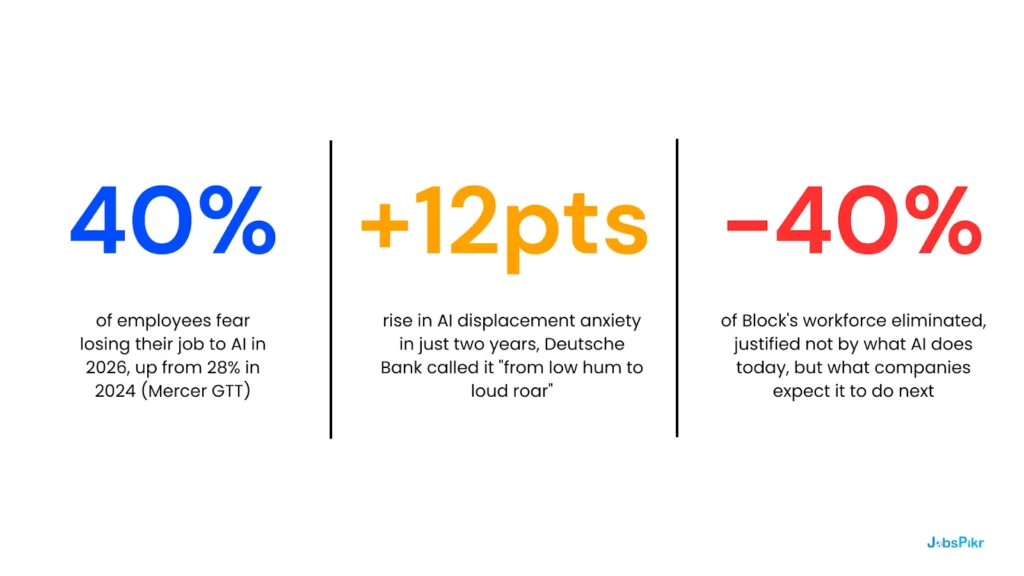

- AI displacement is no longer a background threat: 40% of employees now fear losing their job to AI, up from 28% in 2024, and companies are using the war-economy downturn to accelerate restructuring.

The job market in 2026 was already under pressure before the first bomb dropped. Then, on March 1, 2026, US and Israeli forces launched coordinated strikes against Iranian military infrastructure. Within 72 hours, tanker traffic through the Strait of Hormuz, the narrow waterway through which roughly a fifth of the world’s oil and liquefied natural gas travels, had ground to a near-standstill. Brent crude crossed $90 a barrel. Global shipping companies began quietly rerouting. And an already-fragile job market, still absorbing the aftershocks of federal workforce cuts and an AI-driven restructuring wave, suddenly had one more destabilizing force to absorb.

This wasn’t the job market in 2026 that anyone had forecasted. The International Labour Organization’s Employment and Social Trends 2026 report, published in January, described a world of “fragile stability”, global unemployment holding at 4.9%, masking deep structural weaknesses in job quality, youth employment, and real wage growth. The February US jobs report, released just days after the strikes began, confirmed that fragility in the starkest possible terms.

What makes the current job market in 2026 so consequential for talent intelligence teams, workforce researchers, and HR leaders is not any single data point but the convergence. A geopolitical shock of this magnitude, landing on top of a contracting US labor market, a stalled global hiring recovery, and accelerating AI-driven job displacement, produces compounding effects that official statistics published weeks or months after the fact will be too slow to capture.

“Companies are not hiring in the face of all of these headwinds and uncertainty. And even healthcare is starting to slow down.”

Heather Long

Chief Economist, Navy Federal Credit Union

This report draws on real-time job postings data from JobsPikr, the February 2026 BLS employment report, the ILO Employment and Social Trends 2026 findings, and market analysis from Euronews, Fortune, and the Middle East Council on Global Affairs. What it reveals is the job market 2026 splitting in two and moving faster than any lagging indicator will show.

The US Job Market Was Already in Free Fall Before the First Strike: The February Jobs Report Explains Why

To understand why the Iran conflict is landing so hard on the job market 2026, you first need to understand the ground it landed on. The February 2026 jobs report released by the Bureau of Labor Statistics on March 6, just days after the first US-Israeli strikes, was not a war story. It was a pre-existing condition story. And it was bad.

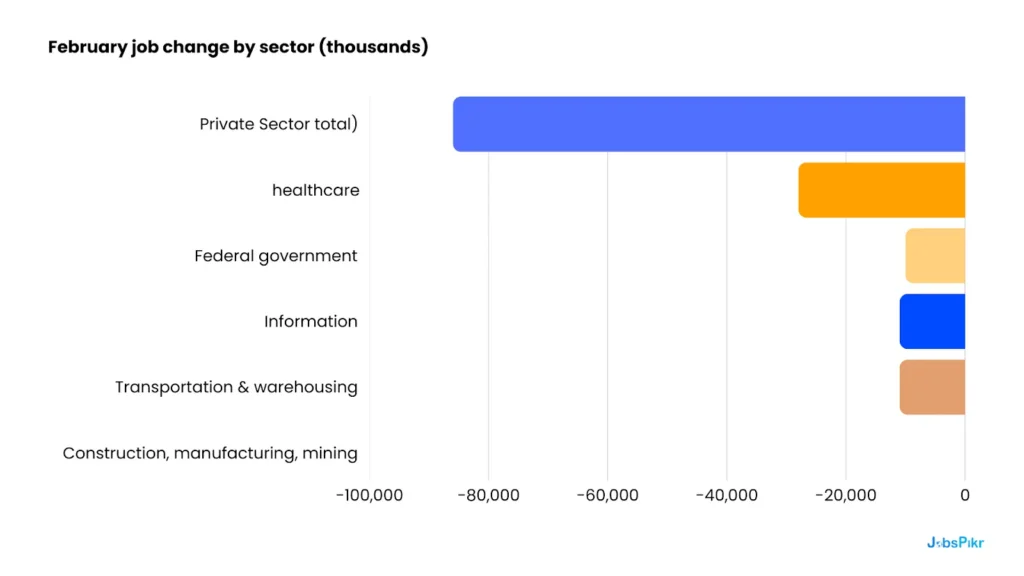

The headline number was the starkest in months, but the details told a more troubling story. Payrolls had now contracted in two of the last three months. December’s report, which had briefly quieted the pessimists, was revised downward into negative territory. And the net job change across the entire US economy since May 2025 stood at just −19,000, meaning nine months of effective stagnation before a single bomb was dropped on Iran.

Sector breakdown: what the February report actually showed

The losses were broad-based, which matters. A broad-based decline signals systemic weakness, not a single-sector event that can be dismissed as temporary noise.

The one-engine economy loses its engine

For most of 2025, the US labor market was sustained by a single sector: healthcare. A San Francisco Fed analysis published in January found that education and health services had driven almost all sustained job growth in 2025, while every other major sector sat flat or in decline. It was a precarious configuration, one engine keeping a heavy plane airborne.

In February, that engine cut out. Healthcare shed 28,000 jobs after adding 77,000 in January, a reversal driven largely by a Kaiser physician strike. As GDP analyst Omair Sharif noted, the report revealed a “labor market so soft that it cannot withstand a strike of 31,000 physicians in healthcare, because no one else is hiring.”

What the “one-engine economy” means for talent intelligence

When a labor market is being held up by a single sector, any disruption to that sector produces a national-level payroll decline even if the underlying cause is temporary. For workforce analysts, this is a critical signal: the absence of hiring breadth is itself a risk indicator. JobsPikr postings data showing sector concentration, the degree to which active hiring is dominated by one or two industries, is a leading warning of exactly this fragility.

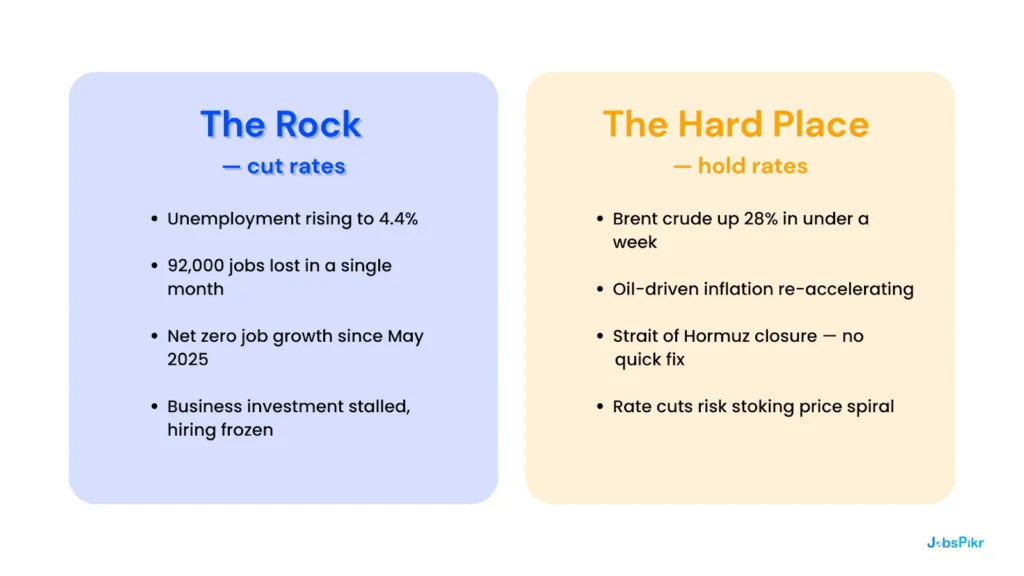

The Fed’s impossible position

The jobs report landed at the worst possible moment for monetary policy. Markets had been pricing in two Fed rate cuts in 2026, a lifeline for businesses weighing hiring and investment decisions. The February data made those cuts more urgently needed from a labor market standpoint. But the Iran conflict, unfolding simultaneously, was doing the opposite: pushing oil prices higher, re-igniting inflation concerns, and making rate cuts harder to justify.

Morgan Stanley’s Ellen Zentner captured the dilemma plainly, describing the Fed as caught between “a rock and a hard place.” Morningstar’s Dominic Pappalardo was more specific: if energy prices keep rising and spark inflation, it will be “much more difficult for the Fed to implement those two forecasted rate cuts in 2026.” For employers already freezing headcount amid uncertainty, the prospect of delayed rate relief is another reason to keep hiring on hold.

“January’s 130,000 gain quieted the pessimists, proving that the labor market had found a floor. February’s data reframes that report as an outlier.”

Christopher Hodge

Chief US Economist, Natixis

The February report, in other words, did not just describe a bad month. It described a structurally fragile labor market, one that had been leaning on a single sector, watching its safety buffers erode, and was now being hit by an external shock of the first order. The Iran conflict did not create the job market 2026 crisis. It accelerated and deepened one that was already forming.

From Chokepoint to Job Market Forecast: How One Strait Is Disrupting Workforces Across Six Industries

Most coverage of the Strait of Hormuz focuses on oil prices. That framing is understandable and incomplete. The strait is not merely an energy chokepoint. It is a global supply chain artery whose disruption reaches semiconductor factories in Taiwan, fertilizer plants in Europe, medical imaging facilities in the United States, and port operations from Rotterdam to Singapore. Each of those downstream effects carries a direct workforce consequence that job postings data is already beginning to reflect.

Frederic Schneider, a senior fellow at the Middle East Council on Global Affairs, described the strait as “the most important global chokepoint for hydrocarbons and fertilisers and a key transshipment hub between Asia and Europe.” Even limited disruption, he noted, can quickly affect prices worldwide. What is happening now is not limited to disruption.

“The most important shockwave is certainly hydrocarbons — not only oil but also natural gas. Energy markets are often the first channel through which geopolitical conflict spreads into the global economy.”

Frederic Schneider

Senior Fellow, Middle East Council on Global Affairs, March 2026

The six industries where workforce impact is already measurable

The supply chain disruption does not distribute itself evenly across the labor market. Some sectors are shedding roles or freezing hiring as operations stall. Others, those positioned to respond to the crisis rather than absorb it, are accelerating demand for skilled workers. The divergence is already visible in job postings data, and it will widen the longer the conflict continues.

The less obvious workforce effects: helium, sulphur, and the hidden supply chains

When analysts model the labor market consequences of an oil price shock, they typically account for energy costs flowing through to transport, manufacturing, and consumer spending. What they rarely model is the cascade through industrial by-products and this is where the 2026 conflict is generating some of its least-anticipated workforce effects.

Helium, produced as a by-product of natural gas extraction, is essential not just for party balloons but for cooling the superconducting magnets in MRI machines and maintaining the inert atmospheres required inside semiconductor fabrication facilities. Qatar accounts for approximately a third of the global supply. A sustained interruption to Qatari gas production or export capacity does not need to be total to create meaningful downstream effects on chip manufacturing timelines and healthcare equipment maintenance, both of which carry their own workforce implications.

Why does this matter for the job market 2026 forecast?

Supply chain shocks of this nature typically take 8–14 weeks to translate into measurable hiring changes in downstream industries, meaning the full job market 2026 impact of the helium and fertilizer disruptions is still arriving. This means the semiconductor and healthcare equipment workforce impact from the helium disruption will not show up in official employment statistics until Q2 or Q3 2026, but it is already visible as a deceleration in job postings growth in affected sectors. This is exactly the kind of leading signal that real-time posting data captures first.

Sulphur presents a parallel case. Produced as a refinery by-product, sulphur is a critical input for phosphate fertilizer manufacturing. A sustained reduction in Gulf refinery output constrains sulphur availability at the precise moment, the spring planting season, when agricultural demand is highest. Schneider flagged this explicitly: “Another shock that may be longer-lasting even if the conflict were to end soon is the fertiliser bottleneck.” Smaller harvests in late 2026 would translate into food price inflation and reduced agricultural employment demand in the world’s most vulnerable economies, a delayed labor market consequence that current forecasting models are not pricing in.

Which Sectors Are Winning and Losing in the 2026 Job Market: A Breakdown by Industry

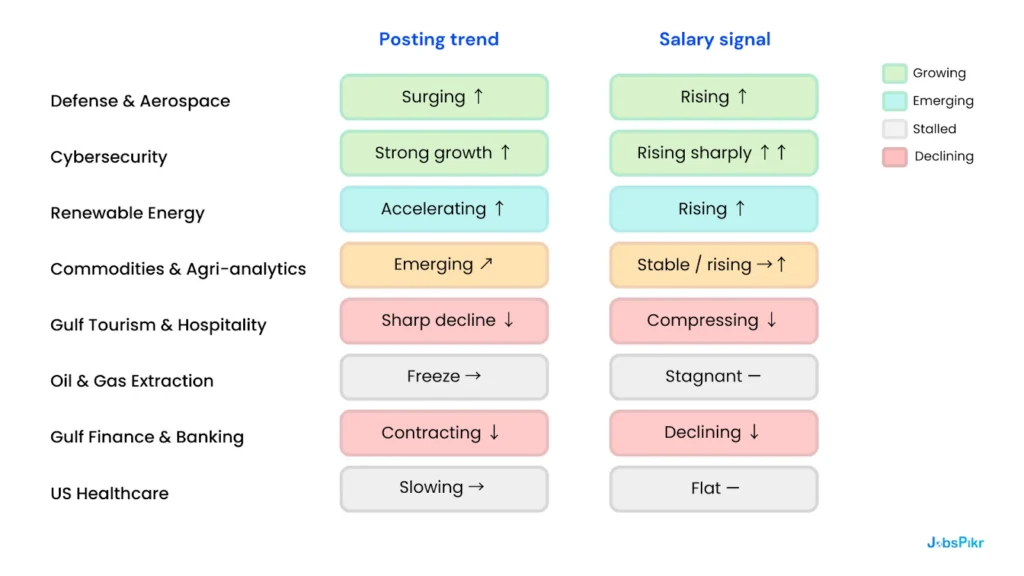

Not every industry is absorbing the shock the same way. The job market in 2026 is not contracting uniformly; it is bifurcating rapidly, with some sectors surging and others collapsing. The US-Israel-Iran conflict is not producing a uniform labor market contraction it is producing a rapid and widening bifurcation. Some sectors are shedding roles, freezing headcount, or watching job postings go dark. Others are posting at the fastest rates in years, pulled upward by the same forces pushing others down. For talent intelligence teams, workforce researchers, and HR leaders, understanding which side of that split your sector sits on is the most operationally urgent question of Q1 2026.

What follows is a sector-by-sector breakdown built from real-time job postings signals, cross-referenced against BLS data, ILO employment trend analysis, and market reporting from the first two weeks of the conflict.

Sectors contracting

Tourism, Travel & Hospitality: A Sharp decline

The Gulf’s tourism and hospitality sector is absorbing the most visible immediate blow. The Iran conflict is estimated to be costing the Middle East travel and tourism industry €515 million per day in lost visitor spending, a figure that translates directly into hotel operations, airline crew, events, and service sector jobs going unfilled or being actively cut. Bookings into Dubai, Riyadh, Doha, and Abu Dhabi have collapsed. Job postings for hospitality roles in the Gulf, which surged through late 2025 on the back of major event calendars and tourism targets, are expected to show a precipitous drop from March 1 onward in the postings data.

Oil & Gas Extraction: Freeze despite high prices

This is the counterintuitive story of the 2026 conflict: oil prices have surged, but upstream oil and gas companies are not translating that into new hiring. The reason is the uncertainty duration. Capital expenditure decisions in oil and gas take months to execute. Companies are not going to staff up new extraction projects in a conflict environment where the price spike may reverse as quickly as it arrived. What job postings data is likely to show is not just a hiring freeze but a rising ratio of expired or closed postings to new ones, roles that were open pre-conflict simply not being refreshed.

Finance & Banking (Gulf-based): Regional contraction

Global banks operating in Gulf financial hubs have tightened physical security and are pausing expansion hiring across the region. Investment banking, trade finance, and private wealth management roles a category that had been growing steadily in Dubai and Riyadh, as both cities positioned themselves as global financial centres, are now on indefinite hold. The workforce effect here is dual: existing staff are being evacuated or relocated, and open positions are being pulled. This is likely to show up in postings data as a near-complete cessation of new role listings from major financial institutions in Gulf metro areas.

Healthcare (United States): Structural slowdown

As detailed in Section 1, the US healthcare’s role as the sole engine of job growth through 2025 is now over at least temporarily. The Kaiser strike effect that drove February’s −28,000 figure may be partially resolved, but the broader hiring slowdown in the sector reflects deeper pressures: federal funding uncertainty, Medicaid review processes, and the same general economic caution suppressing hiring everywhere else. Healthcare is unlikely to recover its role as the labor market’s backstop in the current environment.

Sectors expanding

Defense, Aerospace & Military Contracting: Surging

If there is one unambiguous hiring winner in the 2026 conflict, it is the defense sector. The US-Israel-Iran war has triggered an immediate escalation in defense budget conversations across NATO allies, the Gulf states, and Indo-Pacific partners. Defense contractors, aerospace manufacturers, military logistics firms, and intelligence services are posting at accelerating rates in the US, UK, Israel, and India. This is not a speculative trend; it is already visible in the volume of job postings from the first week of March. Roles spanning systems engineering, UAV operations, electronic warfare, cybersecurity operations, and defense procurement are all showing elevated demand. For talent intelligence teams, defense sector postings are the clearest positive signal in the entire Q1 2026 dataset.

Cybersecurity: Strong growth

Geopolitical escalation and cyber threat activity move in lockstep. State-sponsored cyberattacks typically intensify during and after kinetic military conflicts, pushing enterprise, government, and critical infrastructure security teams to accelerate hiring for roles they had been recruiting slowly. Cybersecurity engineer, threat intelligence analyst, SOC analyst, and incident response specialist postings are among the fastest-growing job categories in Q1 2026, and unlike many defense roles, they are being posted by a broad cross-section of employers, not just dedicated defense contractors. Financial institutions, energy companies, healthcare systems, and technology firms are all competing for the same limited talent pool, which is also pushing median advertised salaries in cybersecurity sharply upward.

Renewable Energy & Green Infrastructure: Accelerating

Every oil price shock in history has accelerated the political urgency of energy transition, and 2026 is no different. Governments in Europe, Asia, and North America are fast-tracking renewable energy investment decisions that had been stalled in budget cycles, using the conflict as political cover to push through spending. The workforce consequence is a surge in postings for solar installation engineers, offshore wind project managers, green hydrogen specialists, battery storage technicians, and energy infrastructure EPC workers. This is one of the few sectors where the conflict is creating durable, long-horizon job growth, not just a temporary spike driven by crisis response.

Commodities Trading & Agricultural Analytics: Emerging demand

Fertilizer disruptions, food price volatility, and supply chain rerouting are creating demand for a category of roles that rarely make headlines: commodities traders, agricultural supply chain analysts, food security strategists, and trade risk specialists. Companies managing global food supply chains and the financial institutions pricing those risks are quietly adding headcount in these areas. This is unlikely to generate large absolute posting volumes, but the growth rate from a low base will be among the highest of any category in Q1 2026 data, making it a useful signal of where the conflict’s second-order effects are landing.

The salary divergence: what the bifurcation looks like in pay data

The sector split is not just a story about job volume; it is a story about pay. The hiring trends of 2026 are producing the sharpest median salary divergence between expanding and contracting sectors in recent memory. Contracting sectors are seeing salary compression or stagnation as competition for roles declines and employers gain leverage. Expanding sectors are seeing advertised salaries rise as employers compete for scarce talent in high-priority fields. The contrast between defense/cybersecurity and hospitality/Gulf energy is likely to be among the starkest median salary divergences visible in postings data for any quarter in the past five years.

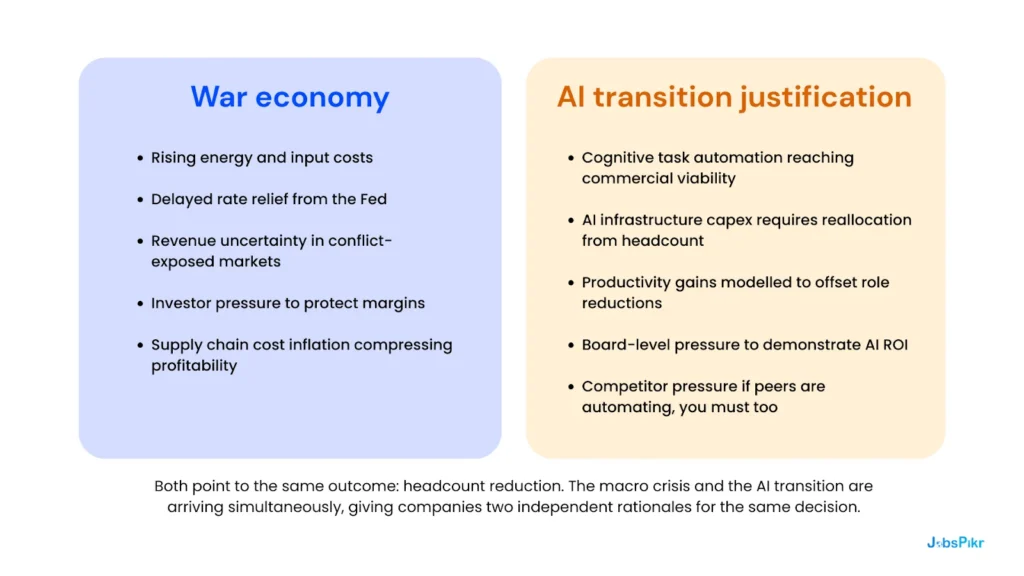

“Job cuts are funding AI expenditures. Headcount reduction is being justified not by what AI can do today, but by what companies expect it to do next — and an uncertain war economy gives them every reason to accelerate that math.”

Brad Conger

Chief Investment Officer, Hirtle Callaghan, March 2026

A note on AI as a force multiplier in contracting sectors

The contraction in white-collar hiring across finance, information services, and professional services is not solely a war effect. Companies in these sectors were already using AI investment as justification for headcount reduction. The conflict gives them additional economic cover to accelerate the restructuring they had already planned. This makes it difficult to disentangle the war’s direct workforce impact from its role as an accelerant of pre-existing automation-driven reduction. Both effects are real; both will be visible in posting data as a simultaneous decline in generalist roles and a rise in AI-adjacent ones.

The Stagflation Risk and What It Means for the 2026 Job Market Forecast

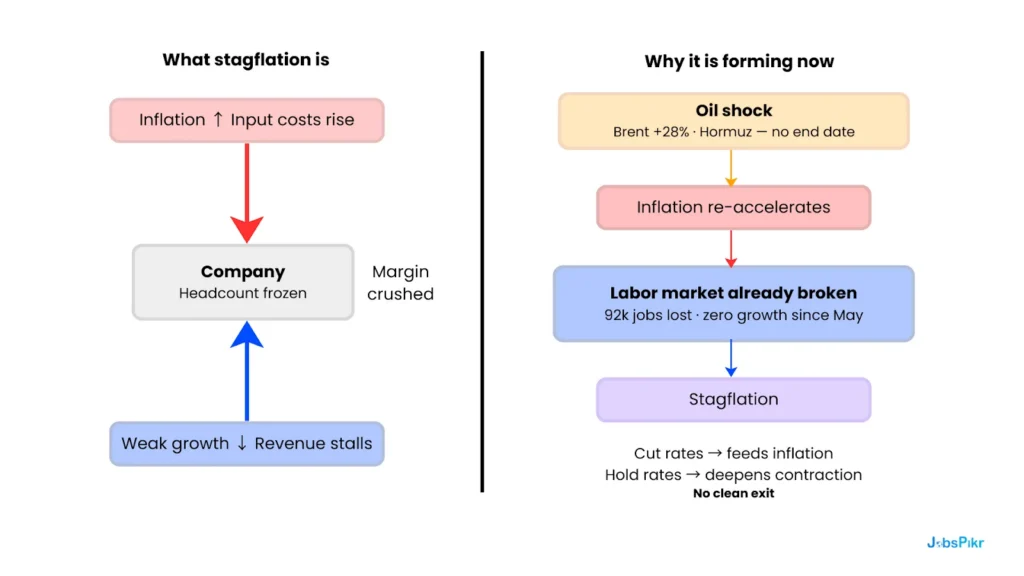

Of all the risks shaping the job market forecast for 2026, stagflation is the most damaging for labor markets and the least well-understood by hiring managers and workforce planners. Stagflation is the rare and brutal combination of high inflation and weak economic growth, and it is the environment in which most conventional workforce planning models simply stop working.

The conditions for stagflation are assembling in real time. What makes the job market 2026 particularly dangerous is that, unlike previous oil shocks 1973, 1979, 2008 this one is landing on a labor market that had already lost its growth engine. There is no buffer. There is no sector generating enough hiring momentum to absorb the shock.

“The worst-case scenario would be an economic slump combined with an interest rate hike to curb inflation. Such a combination could trigger the bursting of asset bubbles and potentially lead to another debt crisis similar to 2008.”

Frederic Schneider

Senior Fellow, Middle East Council on Global Affairs

How stagflation destroys hiring even in sectors that look stable

In a normal inflationary environment, rising prices are accompanied by strong growth, and employers feel confident enough to keep hiring despite higher input costs. In stagflation, the opposite holds: prices rise, but growth stalls, consumer spending weakens, and businesses face a simultaneous squeeze on revenues and costs. The rational employer response, regardless of sector, is to freeze headcount and wait.

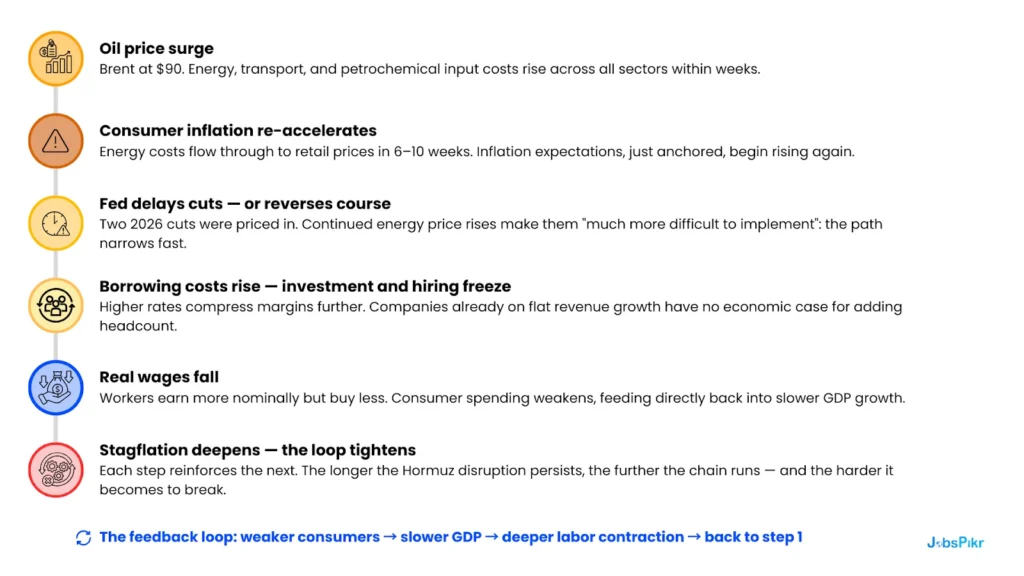

Sustained increases in oil and gas costs feed directly into transport, manufacturing, logistics, and consumer goods pricing within 6–10 weeks. If the Fed responds by holding or raising rates to counter inflation, borrowing costs for businesses rise further, compressing margins and making headcount reduction even more attractive.

Why 2026 is harder to escape than previous oil shocks

The US has significantly increased its domestic energy production since the oil shocks of the 1970s and 2000s, a source of insulation that has been widely cited as a reason not to worry. But the 2026 situation has several features that limit that insulation in ways that matter directly for the labor market:

Four reasons the 2026 shock is harder to absorb

- The labor market entered this shock already weakened. Negative net job growth since May 2025, declining private sector payrolls, and the loss of its only remaining growth engine in healthcare. There is no cushion and no backstop sector ready to absorb displaced workers.

- Global supply chain integration means US companies are exposed regardless of domestic energy production. US manufacturers, logistics companies, and technology firms depend on components, materials, and counterparties exposed to elevated energy costs, even if US oil itself is domestically produced.

- Monetary policy tools are paralysed. The Fed cannot simultaneously cut rates to support the labor market and hold or raise them to contain inflation. The more the conflict persists, the deeper this paralysis becomes, and the longer businesses sit on frozen hiring decisions.

- AI displacement is occurring simultaneously, giving companies both the capability and the justification to reduce headcount permanently. Unlike previous downturns, where companies reduced headcount temporarily and rehired during recovery, companies using this period to fund AI transitions may not return to pre-crisis staffing levels even when conditions improve.

What Stagflation Looks like in Job Postings Data

The stagflation signal in job postings data is distinctive and worth understanding for any talent intelligence team trying to read the Q1 2026 environment accurately. It does not look like a sudden cliff-edge in posting volume. It looks like four concurrent patterns are appearing together:

The Four Stagflation Signals in the Postings Data

Sustained deceleration in new postings

Not a crash, a slow, consistent week-over-week decline in new role listings that began before the conflict and is accelerating after it.

Rising average posting duration

Roles are staying open longer as employers delay commitment to filling them, a proxy for a hiring freeze without formally declaring one.

Salary range compression

Advertised pay bands are narrowing as employers gain negotiating leverage in a softening market, and real wage pressure before it hits payslips.

Sector concentration rising

An increasing share of all active postings concentrated in a smaller number of sectors (defense, cybersecurity, renewables), the two-speed economy is becoming visible in the data.

The weekly job posting velocity since January 2026 is already showing this pattern in the US data, a slow but consistent deceleration that pre-dates the Iran strikes and will accelerate through Q2 if the conflict persists. For workforce planners, the practical implication is direct: the hiring window for competitive roles in contracting sectors is closing faster than official statistics suggest. And for roles in expanding sectors, defense, cybersecurity, and renewables, the talent competition is intensifying faster than most organizations have planned for.

“If we continue to see increasing energy prices sparking inflation concerns, it will be much more difficult for the Fed to implement those two forecasted rate cuts in 2026.”

Dominic Pappalardo

Chief Multi-Asset Strategist, Morningstar Wealth, March 2026

Bottom Line for Talent Intelligence Teams

Stagflation is not a future risk to model; it is a present condition to navigate. Any job market forecast for 2026 built on the standard cycle of downturn-then-recovery is now outdated: companies using this period to fund AI transitions and permanent restructuring will not return to pre-crisis headcount levels when the conflict eventually resolves. Workforce plans built on historical recovery patterns need to be stress-tested against a scenario in which the recovery looks different, with fewer roles, higher skills requirements, and a permanently bifurcated market between sectors that benefited from the crisis and those that were structurally reshaped by it.

The AI Displacement Amplifier: How the War Economy Is Accelerating Structural Job Losses

The job market 2026 is not facing one disruption. It is facing two simultaneously, and they are reinforcing each other in ways that no single headline is fully capturing. The US-Israel-Iran conflict is a cyclical shock: acute, external, and potentially temporary. AI-driven displacement is a structural shift: gradual, internal, and accelerating, regardless of what happens in the Strait of Hormuz. The dangerous dynamic of 2026 is that the war economy is giving companies the economic and political cover to accelerate structural changes they had already planned.

Employee fears of losing their job to AI jumped from 28% in 2024 to 40% in 2026, according to Mercer’s Global Talent Trends survey. Deutsche Bank analysts predicted in January that this anxiety would go “from a low hum to a loud roar” this year, a forecast that has since been overtaken by events. The mechanism is not straightforward for AI replacement of jobs today. It is more precisely described by Brad Conger, Chief Investment Officer at Hirtle Callaghan: AI isn’t replacing jobs yet, but job cuts are funding AI expenditures. Headcount reduction is being justified not by what AI can do today, but by what companies expect it to do next.

“Job cuts are funding AI expenditures. Block’s decision to eliminate 40% of its workforce fits the pattern — headcount reduction justified not by what AI can do today, but by what companies expect it to do next.”

Brad Conger

Chief Investment Officer, Hirtle Callaghan, March 2026

The dual justification problem is why this downturn is different

In previous economic downturns, companies reduced headcount to cut costs and restored it when conditions improved. The recovery was relatively predictable. The 2026 downturn has a feature that makes this recovery less automatic: the companies doing the cutting are simultaneously investing the savings into AI infrastructure. Once that transition is funded and partially complete, the economic case for rehiring at pre-crisis levels disappears, and the AI capability has replaced the need.

Both sets of justifications are landing on the same conclusion: reduce headcount now. For public companies, the war economy provides a defensible external narrative. For their shareholders, the AI transition provides a credible long-term story. The workers whose roles sit at the intersection of both pressures, white-collar generalists in finance, professional services, information technology, marketing, and legal, are facing compounding rather than sequential risk.

What this looks like in the postings data

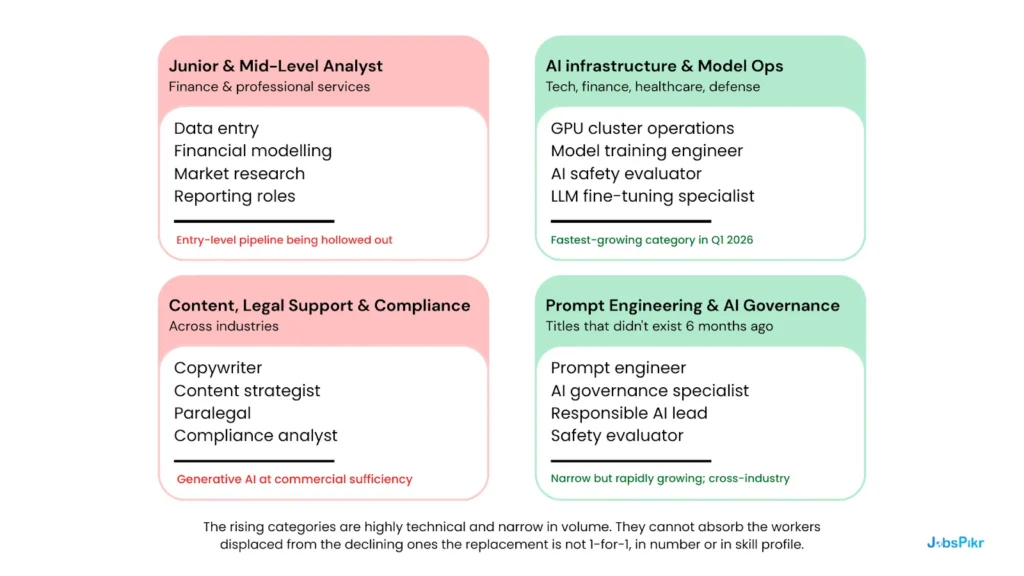

The AI displacement signal in job postings data has a distinctive fingerprint: falling volume in generalist white-collar roles alongside rising volume in AI-adjacent roles in the same sector. Finance is seeing fewer junior analyst postings but more ML engineer postings. Legal is seeing fewer paralegal postings but more legal AI specialist postings. When that divergence accelerates in a period of macroeconomic stress, as it is now, it confirms that restructuring is structural, not cyclical. Companies will not rehire the eliminated roles when conditions improve; they will scale the AI capabilities those roles helped fund.

Where the AI-displacement effect is most visible in the job market

The sectors showing the clearest dual signal, total postings falling while AI/automation role postings rise, are precisely the white-collar categories that Anthropic’s January 2026 research identified as most exposed to cognitive task automation. Blackrock CIO Rick Rieder noted that AI-driven productivity gains are “unequivocal” and that cognitive technology is replacing cognitive thinking, but the labor-intensive reinvestment in manufacturing and physical sectors needed to absorb that displacement has not materialised at scale. Construction, manufacturing, and mining were all flat in February. The new investment is going into AI infrastructure, not into the physical economy that would generate replacement employment.

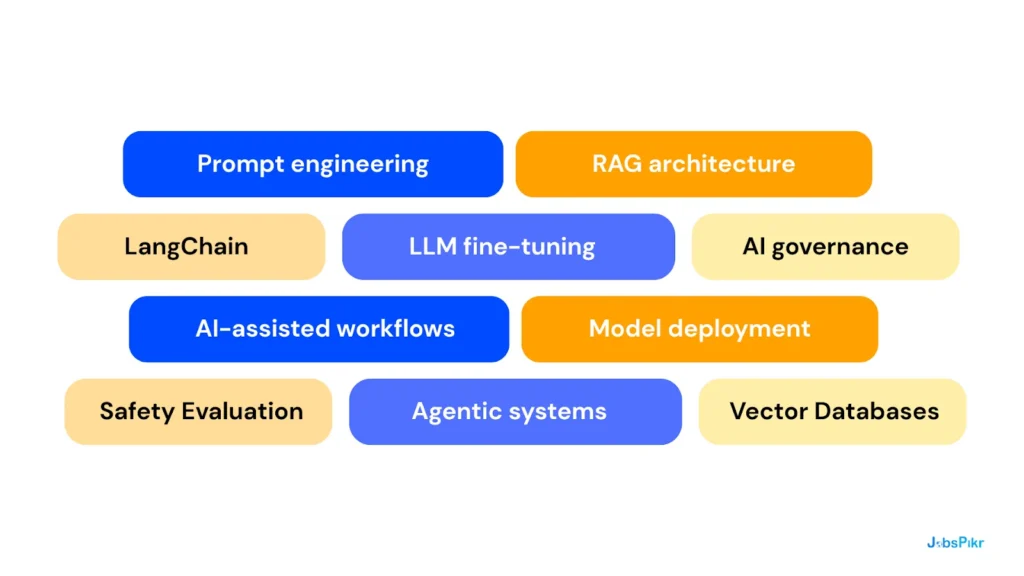

The fastest-growing skills in job descriptions: Q1 2026

The skill-level signal is even more granular than the role-level signal. The skills growing fastest in frequency across all US job descriptions in Q1 2026 paint a precise picture of where employer investment is going, regardless of what sector the job sits in.

The concentration of this skill demand in a narrow talent pool means there are far fewer people with these competencies than companies are seeking, which is driving compensation significantly higher for AI-adjacent roles even as the broader market compresses. For talent intelligence teams monitoring salary trends, the divergence between AI-infrastructure compensation and generalist-role compensation is widening every week in Q1 2026 data.

What does this mean for the job market forecast through 2026?

The intersection of war economy and AI displacement creates a job market 2026 with no clean historical precedent. The 1970s stagflation playbook does not account for simultaneous structural technological displacement. The 2008 financial crisis playbook does not account for a commodity shock layered on top of automation pressure. Standard models assume that cyclical downturns are followed by cyclical recoveries companies hire back the roles they cut when growth returns.

That assumption is now in question. Companies using this downturn to fund AI transitions will not return to pre-crisis headcount levels even when economic conditions improve because the transition will already be complete. The roles eliminated in early 2026 will not be reposted in 2027. They will be replaced by a smaller number of higher-skill, higher-compensation AI-adjacent roles, and a larger number of people will be seeking employment in a market that has permanently reduced its capacity to absorb them at their previous level.

“AI-driven productivity gains are unequivocal. But labor-intensive reinvestment in manufacturing, real estate, and semiconductor production has to happen to absorb the displacement. That reinvestment hasn’t materialised at scale.”

Rick Rieder

Chief Investment Officer of Global Fixed Income, Blackrock

Global Divergence: Which Regions Are Hardest Hit in the 2026 Labor Market

The Iran conflict does not affect every labor market equally. The ILO’s Employment and Social Trends 2026 report described global labor markets as showing “fragile stability” even before the conflict began, but fragile stability conceals a world of fundamentally different regional realities. The war has sharpened those differences into a clear and measurable divergence. Some regions are in the direct path of the shock. Others are positioned to absorb displaced activity and may actually benefit in narrow ways. A third group faces second-order effects, fertilizer disruptions, food price inflation, and trade cost increases that will materialise slowly but prove the most durable.

Gulf States: UAE, Qatar, Saudi Arabia, Kuwait, Bahrain

The Gulf economies are absorbing the conflict on every front simultaneously, and the labor market data reflects that multiplicity. Tourism and hospitality hiring has collapsed. Gulf-based financial institutions have frozen regional expansion. Logistics and shipping roles dependent on Hormuz transit have dried up. And despite elevated oil prices, energy sector hiring is frozen as companies defer capital expenditure decisions pending resolution of the conflict.

The UAE has stated publicly that it will oppose Iran’s actions and can withstand the shock, and its economic diversification gives it more resilience than some Gulf neighbors. But job postings data tells an unambiguous story: active listings across all major Gulf employment categories began declining sharply in the week of March 1 and have not recovered. The Gulf labor market is, for the first time since the post-COVID recovery, contracting across all major sectors simultaneously rather than rotating weakness from one category to another.

International talent that had been relocating to Dubai and Riyadh, attracted by tax advantages, infrastructure investment, and a booming financial services sector, is now reassessing. Global banks that had been building Gulf hub capacity are pausing hiring. The workforce consequence of conflict is not only the direct jobs lost; it is the pipeline of future roles that is no longer being built.

- Hospitality postings: sharp weekly decline from Mar 1

- Finance hiring: frozen in Dubai, Riyadh, Doha

- Energy sector: hiring freeze despite $90 oil

Europe: Germany, Netherlands, Poland, Belgium, Southern EU

Europe’s vulnerability is structural, not incidental. The continent spent 2022–2025 rebuilding its energy supply chains after the loss of Russian gas, a process that increased reliance on Middle Eastern LNG precisely as a conflict in that region has disrupted those supply lines again. The result is a labor market absorbing an energy cost spike on top of an already-fragile industrial outlook.

The ILO’s trade uncertainty analysis is directly relevant here. When trade policy uncertainty rises, and it has risen significantly in 2026 across tariffs, conflict risk, and shipping cost volatility, real wages in supply-chain-integrated economies face measurable downward pressure. The ILO estimates falls of up to half a percentage point per year in wages in the most affected regions. Compounded over time, this is significant for economies already facing demographic-driven labor force contraction.

Germany’s energy-intensive manufacturing sector, the Netherlands’ logistics and chemicals industry, Belgium’s petrochemical sector, and Eastern European manufacturing hubs supplying German industrial chains are all facing elevated input costs with limited ability to pass them through to customers. Hiring in these sectors was already slowing in Q4 2025; it is now decelerating further. The sectors most exposed are chemicals, steel, glass, fertilizer production, and heavy manufacturing, none of which are hiring freely in the current environment.

- Manufacturing hiring: decelerating across the DACH region

- Chemicals & petrochemicals: input cost freeze

- Logistics hubs: Rotterdam absorbing Gulf rerouting but at a higher cost

East Asia: Japan, South Korea, Taiwan, China

East Asia’s exposure runs through two channels that reinforce each other: LNG dependency and helium supply concentration. Japan and South Korea rely on Middle Eastern LNG for a significant share of industrial and residential energy. Higher energy costs flow directly into manufacturing cost structures, affecting the competitiveness of export-oriented manufacturers and creating pressure to reduce workforce costs rather than expand them.

The helium channel is potentially more disruptive and less widely recognised. Taiwan, South Korea, and Japan are home to the world’s most advanced semiconductor fabrication, a process that requires helium as an inert carrier gas in cleanroom environments. Qatar’s helium supply, roughly a third of global production, is being disrupted by the same gas infrastructure constraints affecting LNG exports. The workforce effect will be delayed, as noted in Section 2, the 8–14 week lag means the impact on fab operations and tech sector hiring will not be measurable in official statistics until Q2 2026.

The ILO data adds important context: the major improvements in global work quality over the past decade have been driven by Asia, first China, now India. Any shock that slows regional economic momentum disproportionately affects global progress on informality, working poverty, and wage growth, because Asian improvements have been the primary driver of positive global aggregate trends.

- Semiconductor jobs: helium supply pressure building, lag effect Q2

- Manufacturing: energy cost pressure on workforce planning

- Export competitiveness: input cost inflation compressing margins

United States: Partially insulated, selectively exposed

The US enters the conflict with the most resilience, domestic energy production has reduced the direct oil price pass-through significantly compared to the 1970s shocks. The defense sector hiring surge is a real and substantial counterweight to the broader labor market weakness. And the US dollar’s reserve currency status provides a monetary buffer that few other economies enjoy.

But “partially insulated” is not the same as “unaffected.” The February jobs report demonstrated that the labor market was already contracting before the first strike. The stagflation dynamics described in Section 4 apply regardless of domestic energy production, oil-driven inflation affects every economy that participates in global trade, which the US does at scale. And the AI displacement pressure described in Section 5 is most acute in the US, where the largest technology companies and the most advanced AI deployment are headquartered.

The net picture for the US job market forecast is one of sharp bifurcation, stronger than almost any other major economy in the expanding sectors (defense, cybersecurity, renewable energy), but no more protected than peers in the contracting ones (white-collar generalist roles, Gulf-exposed financial services, AI-displaced professional services).

- Defense hiring: strongest positive signal in Q1 dataset

- White-collar contraction: AI + war economy dual pressure

- Fed paralysis: rate cut delay compounds hiring freeze

South & Southeast Asia: India, Vietnam, Bangladesh, Indonesia

South and Southeast Asia occupy the most complex position in the regional picture, simultaneously facing real risks and capturing genuine opportunities created by the conflict’s supply chain disruptions. The India growth story, which the ILO data identifies as now the primary driver of global work quality improvement, is both resilient and exposed in different parts of the economy.

The opportunity channel runs through supply chain diversification. Companies that had been gradually shifting manufacturing and services away from China, the “China+1” strategy that accelerated post-pandemic, are finding the Gulf conflict adds further urgency to that diversification. India’s manufacturing sector, Vietnam’s electronics assembly industry, Bangladesh’s garment production, and Indonesia’s resource processing are all positioned to absorb some of the supply chain rerouting. Job postings for manufacturing, logistics, and operations roles in these countries have been tracking upward through Q1 2026, and the conflict may accelerate that trend.

The risk channel, however, is real. The ILO’s trade uncertainty analysis shows that real wage pressure is most acute in supply-chain-integrated lower-income economies precisely because they have the least buffer. When trade costs rise and global demand softens, it is the workers at the base of the global supply chain, earning the lowest wages, with the least formal employment protection, who absorb the first and deepest wage compression.

- India manufacturing: absorbing China+1 rerouting, Q1 postings rising

- Vietnam & Bangladesh: electronics and garment supply chain gains

- Real wage risk: trade uncertainty hitting base-of-chain workers hardest

Africa & Low-Income Economies: The Delayed Catastrophe

The most severe human workforce consequence of the Iran conflict will not show up in the Q1 2026 job postings data. It will arrive in Q3 and Q4, in the form of smaller harvests, higher food prices, reduced agricultural employment income, and increased working poverty across sub-Saharan Africa and parts of South Asia. The mechanism is the fertilizer disruption described in Section 2, and the ILO’s 2026 baseline makes clear why this matters so acutely.

The fertilizer bottleneck is arriving at the worst possible moment. The spring planting season is underway in many parts of the world right now. Reduced fertilizer availability during planting, due to sulphur supply constraints from Gulf refinery disruption, translates into smaller harvests later in the year. Smaller harvests translate into higher food prices. Higher food prices translate directly into reduced real income for agricultural workers and smallholder farmers who make up the majority of the working-age population in sub-Saharan Africa and parts of South Asia.

As Frederic Schneider noted, this is a shock “that may be longer-lasting even if the conflict were to end soon”, because the agricultural production cycle means the consequences will unfold over a six-to-nine-month period regardless of when the Strait of Hormuz reopens. The job market impact in these regions is not measurable yet. But it is already in motion, and it will be the most enduring workforce consequence of a conflict that most global labor market analysis is treating as primarily a story about energy prices and Gulf business sentiment.

- Fertilizer supply — disrupted at planting season

- Agricultural employment — at risk Q3 2026

- Working poverty — trajectory reversing

ILO context: Fragile Stability Beneath The Headline Number

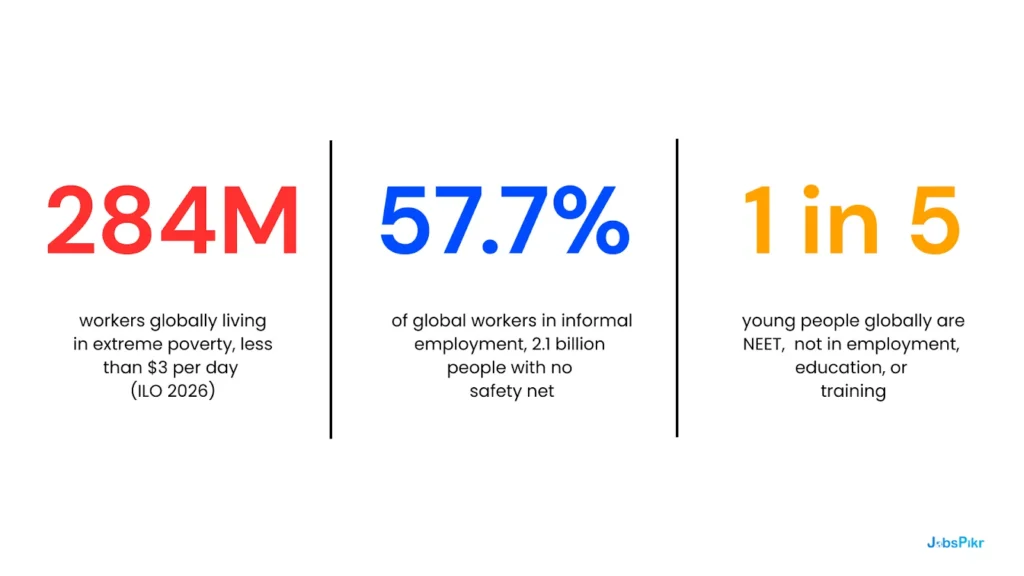

The ILO’s Employment and Social Trends 2026 report found that globally, 57.7% of workers, approximately 2.1 billion people, are in informal employment, with no social protection, no formal employment relationship, and no buffer against economic shocks. Progress on reducing informality had already stalled before the conflict. The Iran war is not creating this vulnerability, but it is stress-testing it at precisely the moment when the buffers are thinnest.

“Stable labour markets are not necessarily healthy labour markets. There are major challenges underneath — and where progress is too slow.”

Stefan Kühn

Senior Economist, ILO Research Department, January 2026

What Talent Intelligence Teams Should Be Watching Right Now

The preceding six sections have mapped the landscape of the 2026 conflict’s workforce impact. This final section is for the practitioners, talent intelligence analysts, HR leaders, workforce researchers, and people analytics teams who need to translate that landscape into actionable signals. The core argument is simple: in a market moving at this speed, organizations relying on official labor statistics are operating with a structural information disadvantage.

The Bureau of Labor Statistics publishes payroll data with a multi-week lag. Eurostat and national statistics agencies across Asia publish even later. By the time official data confirms what real-time postings data is already showing, hiring decisions will have been made, roles will have been frozen, and the competitive window for talent acquisition in expanding sectors will have narrowed significantly.

The Leading Indicator Gap

The February 2026 jobs report showed what happened in payrolls through the end of February, but job postings data showed the healthcare sector’s deceleration in early February, weeks before the BLS counted the payroll drop. The same leading relationship applies to the post-March 1 effects: postings data is showing the defense surge, the Gulf hospitality collapse, and the cybersecurity demand spike right now. Official statistics will confirm these trends in April and May. The question for talent intelligence teams is whether they want confirmation or warning.

Seven Signals to Track Through Q2 2026

1. Defense & aerospace posting velocity weekly, by country

Track US, UK, Israel, and India defense postings week-over-week from March 1. This is the clearest positive hiring signal in the entire Q1 2026 dataset and the one most likely to shift workforce planning decisions in adjacent industries. A sustained surge beyond 6–8 weeks signals structural budget reallocation, not just crisis-response hiring.

2. Gulf hospitality & logistics weekly collapse rate from March 1

The steepness and duration of the Gulf posting decline will determine whether this is a temporary shock or a structural relocation of regional economic activity. If postings in the UAE and Qatar do not recover within 4–6 weeks of any ceasefire, it signals permanent reallocation of investment and talent to alternative hubs.

3. Cybersecurity median salary trend is not just volume

Volume alone understates the story. The combination of rising postings and rising median advertised salary in cybersecurity signals a genuine demand/supply imbalance. When salary rises alongside volume, it means employers are competing, not just posting speculatively. Track this monthly through Q2 to identify the compensation ceiling before it hardens.

4. AI-adjacent roles as a % of total postings per sector

The ratio of AI/automation postings to total postings is the most direct measure of how quickly companies are using the war economy downturn to fund structural transitions. Track this ratio in finance, professional services, and healthcare, specifically, these are the sectors where the dual justification problem of Section 5 is most acute.

5. Geographic hiring pivots: Gulf hubs vs. alternative cities

Track active postings in Dubai, Riyadh, and Doha against Singapore, Mumbai, Amsterdam, and London for finance, logistics, and operations roles. A sustained divergence, Gulf declining while alternative hubs rise signals that companies are not pausing hiring but permanently relocating their talent acquisition geography. This is the earliest signal of a long-term structural shift in where global talent demand sits.

6. Renewable energy job postings by country, growth rate ranking

Pull solar, wind, green hydrogen, and battery storage postings for the US, Germany, India, and Australia. Rank by growth rate against Q4 2025 to identify which governments are translating energy security urgency into actual workforce investment fastest. This is a leading indicator of where long-horizon engineering and project management talent demand will concentrate through 2026 and 2027.

7. Unique employer count per sector, not just posting volume

A contraction in the number of distinct employers actively hiring signals systemic sector-wide caution, not just a single company pulling back. Track unique employer count in Gulf-exposed sectors (hospitality, logistics, oil & gas) and compare to expanding sectors (defense, cybersecurity, renewables). When the employer count diverges as sharply as posting volume, it confirms the bifurcation is structural rather than concentrated in a handful of large organisations.

The Intelligence Imperative for 2026

The job market 2026 is not a market that rewards patience. It is a market where the window for competitive talent acquisition in expanding sectors is measured in weeks, where hiring freezes in contracting sectors are deepening faster than any official statistic will show, and where the structural transformation driven by AI is accelerating under the cover of a war economy that gives every company the justification it needs to act decisively.

The organisations that will navigate the job market in 2026 most effectively are those with access to real-time, granular job postings data, not to predict the future, but to see the present clearly while their competitors are still waiting for last month’s official reports to confirm what the market moved past three weeks ago. In 2026, the leading indicator is not a forecast. It is the hiring signal that employers are already broadcasting, in real time, in every job posting they open and every one they quietly let expire.

JobsPikr’s Real-time Labor Market Intelligence

JobsPikr aggregates real-time job postings from across 50+ countries, covering sector-level trends, median salary signals, geographic hiring shifts, and skill demand velocity. Built for talent intelligence teams, workforce researchers, and HR technology platforms that need to act before official labor statistics catch up.

References:

- Primary News & Market Sources

- Fortune — “The abysmal February jobs report shatters hopes of a labor market recovery for 2026 and leaves the Fed ‘between a rock and a hard place'” — Eva Roytburg, March 6, 2026

- Euronews — “Markets may be underestimating how the Iran war could hit the global economy” — Mohamed Elashi, March 16, 2026

- Euronews Travel — “Iran conflict costs Middle East travel and tourism industry €515 million a day” — March 11, 2026

- CNBC — “Jobs report, Trump, Iran-Israel war, economy” — March 6, 2026

- Reuters — “Wall St futures slip as Middle East conflict rages, jobs data in focus” — March 6, 2026

- Investopedia — “Why the Year 2026 May Present Tough Times for Both Job Hunters and Employers” — 2026

- Institutional & Research Reports

- International Labour Organization (ILO) — Employment and Social Trends 2026 (Flagship Report) — January 2026

- ILO Future of Work Podcast — Episode 81: “Global employment in 2026: A fragile stability” — Stefan Kühn & Marva Corley-Coulibaly, January 22, 2026

- Mercer — Global Talent Trends 2026 — AI displacement anxiety data (28% → 40%)

- Deutsche Bank Research — AI job anxiety analysis: “from a low hum to a loud roar” — January 2026

- Federal Reserve Bank of San Francisco — “Recent Slowdown in Labor Supply and Demand” — Economic Letter, January 2026

- Bureau of Labor Statistics (BLS) — The Employment Situation — February 2026 — Released March 6, 2026

- Anthropic Research — AI job displacement mapping report — January/March 2026 (referenced in Fortune, March 6, 2026)

- Analyst & Expert Commentary

- Heather Long, Chief Economist, Navy Federal Credit Union — February jobs report commentary, March 6, 2026 (via X / Fortune)

- Frederic Schneider, Senior Fellow, Middle East Council on Global Affairs — Euronews interview on Hormuz economic risk, March 16, 2026

- Dominic Pappalardo, Chief Multi-Asset Strategist, Morningstar Wealth — Fed rate cut commentary, March 2026 (via Fortune)

- Ellen Zentner, Morgan Stanley — “Rock and a hard place” Fed commentary, March 2026 (via Fortune)

- Christopher Hodge, Chief US Economist, Natixis — “Fool’s gold” labor market commentary, March 2026 (via Fortune)

- Brad Conger, Chief Investment Officer, Hirtle Callaghan — AI/job cuts framework, March 2026 (via Fortune)

- Rick Rieder, Chief Investment Officer of Global Fixed Income, Blackrock — AI productivity and displacement commentary, March 2026 (via Fortune)

- Omair Sharif, GDP analyst — Healthcare labor market commentary, March 2026 (via Fortune)

- Stefan Kühn, Senior Economist, ILO Research Department — Employment and Social Trends 2026, January 2026

- Marva Corley-Coulibaly, Senior Economist & Trade Expert, ILO — Trade uncertainty and labor market commentary, January 2026

- Sector & Investment Analysis

- Jarvis Invest — “Top Sectors to Watch Now in 2026 During Global Geopolitical Shifts” — Sumit Chanda, March 15, 2026

FAQs

How is the Iran war affecting the job market in 2026?

The Iran war is creating a two-speed job market in 2026. The US-Israeli campaign has paralyzed the Strait of Hormuz, pushing Brent crude from $70 to $90 a barrel and triggering immediate hiring freezes in Gulf logistics, hospitality, trade finance, and oil & gas. Simultaneously, defense, cybersecurity, and renewable energy sectors are surging as governments accelerate security and energy transition spending.

What is the US job market forecast for 2026?

The US job market forecast for 2026 is one of sharp bifurcation. The economy lost 92,000 jobs in February before the Iran conflict began, the worst monthly decline since October 2025, with unemployment rising to 4.4%. Defense, cybersecurity, and renewable energy are the bright spots. White-collar services, healthcare, and Gulf-exposed industries face continued contraction through Q2.

Which sectors are hiring during the 2026 Middle East conflict?

The sectors actively hiring in the job market 2026 despite the Middle East conflict are defense and aerospace, cybersecurity, renewable energy, LNG infrastructure, and commodities trading. Defense and cybersecurity are posting at the fastest rates since the conflict began, driven by accelerating government spending and a surge in state-sponsored cyber threat activity targeting enterprises globally.

How do oil price shocks impact employment?

Oil price shocks raise transport, manufacturing, and logistics costs across the economy within 6–10 weeks, squeezing business margins and triggering hiring freezes. If central banks respond by holding or raising interest rates to contain inflation, as the Fed faces in the job market in 2026, borrowing costs rise further, compressing investment and deepening the employment contraction into stagflation conditions.

What industries are projected to grow the most in the US job market by 2026?

In the US job market in 2026, the industries projected to grow most are defense and aerospace, cybersecurity, renewable energy, and AI infrastructure. The Iran conflict has accelerated growth in the first three by increasing geopolitical and energy security urgency. AI infrastructure roles are growing independently as companies fund automation transitions, even as total hiring volume in most other sectors declines.

What impact would a regional conflict have on global supply chain jobs?

A regional conflict like the Iran war demonstrates exactly how supply chain job disruption spreads globally through the job market in 2026. Hormuz disruption has frozen Gulf port and logistics hiring, threatened semiconductor jobs through helium supply constraints, and put agricultural employment at risk through fertilizer shortages. Jobs do not disappear; they shift geographically to rerouted hubs like Singapore, Rotterdam, and Houston.

What are the top job sectors in the US influenced by the Iran war?

The US sectors most directly influenced by the Iran war in the job market 2026 are defense contracting, cybersecurity, energy infrastructure, and LNG operations, all seeing hiring surges. On the contracting side, oil & gas extraction, Gulf-exposed finance, and white-collar professional services are all under pressure from the combined impact of geopolitical uncertainty, stagflation risk, and accelerating AI-funded restructuring.

Are there online platforms tracking job market changes related to the Iran war?

Yes. JobsPikr is a real-time job postings intelligence platform that tracks hiring changes across 50+ countries, making it one of the most effective tools for monitoring how the Iran conflict is reshaping the job market in 2026. Unlike official labor statistics, which lag 4–6 weeks, JobsPikr surfaces sector-level hiring surges and collapses, in defense, Gulf logistics, cybersecurity, and renewables, as they happen, giving talent intelligence teams, HR leaders, and workforce researchers the earliest available signal of where the market is moving.